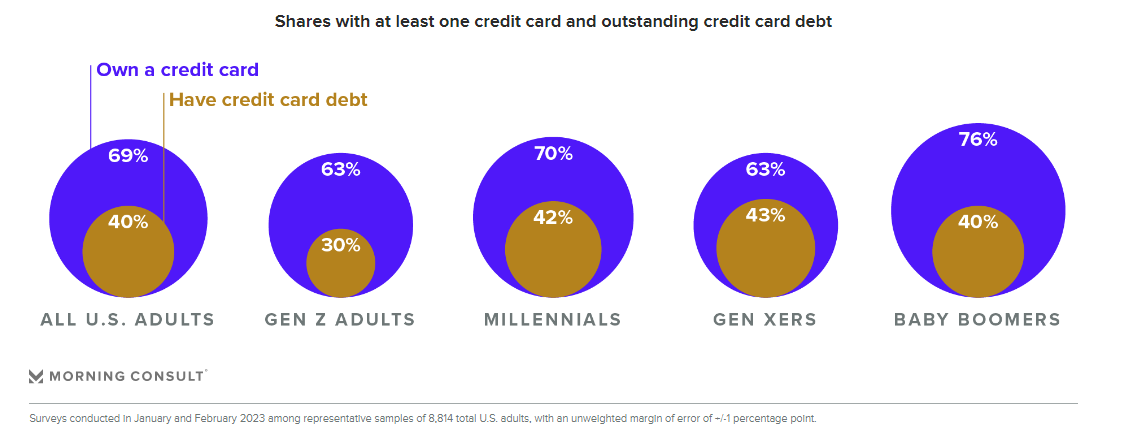

- 30% of Gen Z adults report having credit card debt, at least 10 percentage points lower than older generations.

- There is a common misconception that young adults are wary of credit cards, but Gen Z adults are about as likely to have them as the general population.

- Despite their healthy relationship with credit cards, Gen Zers are still worried about their financial future.

All U.S. consumers are grappling with inflation, but the country’s youngest adults are doing so while also trying to establish their financial footing. While this certainly presents challenges for Gen Z adults, recent Morning Consult data indicates that when it comes to credit, the kids are all right: Not only are Gen Z adults accessing credit through credit cards at the same pace as older generations, but they’re managing their debt better, too.

Gen Z adults are not credit-shy

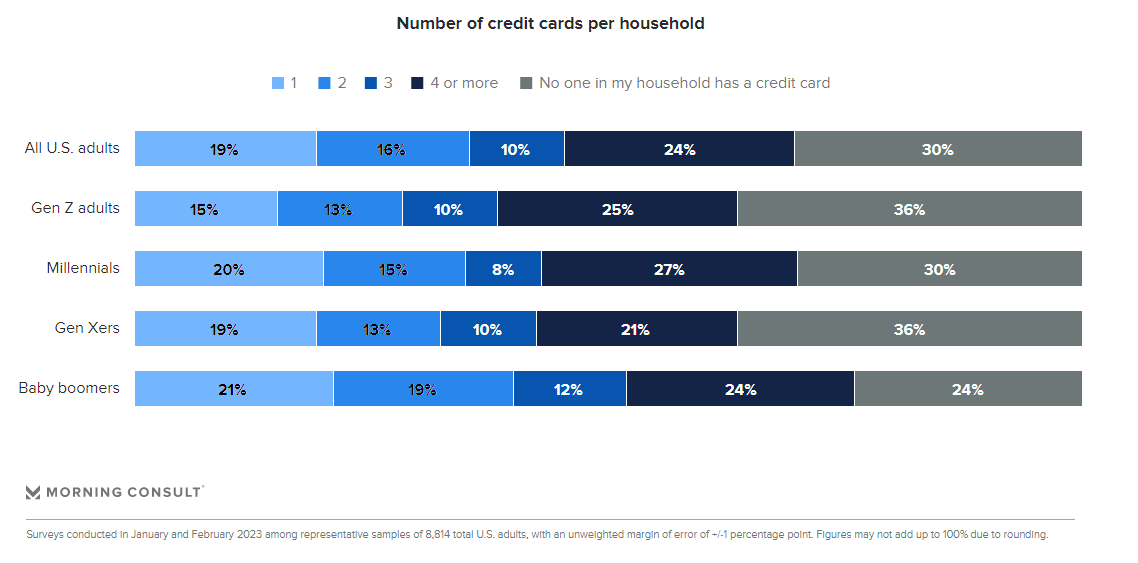

There’s a misconception that younger adults are reluctant to use credit cards. This narrative originated after the Great Recession, when millennials were the youngest adult generation, but it has been extended to Gen Z as they have entered adulthood. However, as of early 2023, Gen Z adults’ use of credit cards is on par with their Gen Xer parents: 63% of each generation own at least one credit card, and the majority of credit card owners report that they have more than one.

A lot has happened since millennials were the youngest adult generation and were said to be shying away from credit. The Credit Card Accountability Responsibility and Disclosure Act of 2009 limited the marketing and issuing of credit cards to young adults. Additionally, millennials emerged from the Great Recession’s high unemployment and entered midlife and parenthood, life stages that are associated with more expenses and a greater need for credit. Gen Zers, by contrast, are entering adulthood without being bombarded by credit card offers the way millennials were, with a heightened understanding of the dangers of credit card debt after seeing its impact on older generations, and in the midst of a tighter labor market that can make responsible credit use much more achievable and less daunting.

Less than a third of Gen Z adults have credit card debt

Compared with other generations, Gen Z adults are less likely to say they have outstanding credit card debt. Less than a third of Gen Z adults (30%) report having any credit card debt, meaning most are not carrying an outstanding balance on their cards from month to month. This is a considerably smaller share than the roughly 40% of millennials, Gen Xers and baby boomers who report the same.

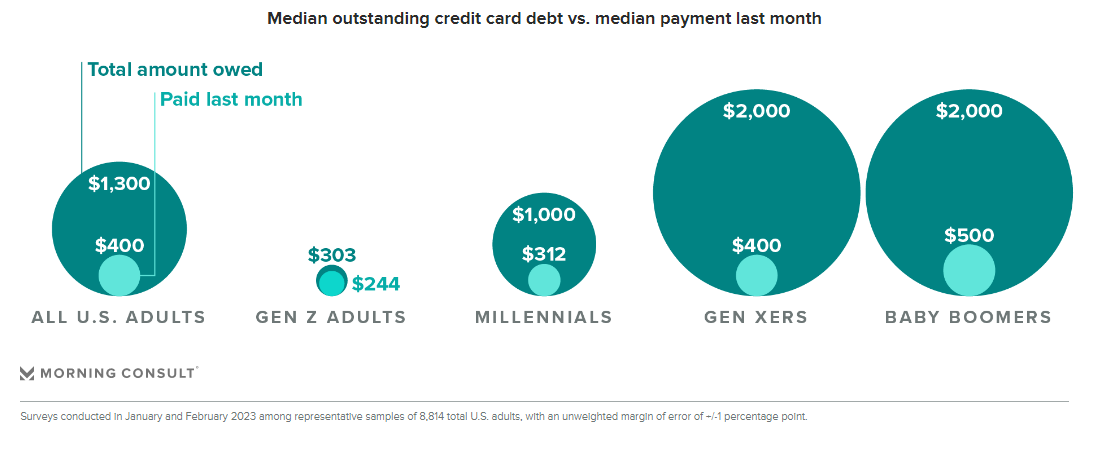

Not only are Gen Z adults less likely to have any credit card debt, but the debt they do have is much lower than that of older generations. The median credit card payment for the months of January and February was $400 for all U.S. adults; boomers’ median payment was higher at $500, and Gen Z adults’ was roughly half that at $244. These young adults aren’t just chipping away at their outstanding balance each month — they’re also prioritizing paying off their entire credit card debt more than older generations. Gen Z’s median outstanding credit card debt is $303, so their $244 median monthly payment covers nearly all of their debt. The same isn’t true of older generations, for whom the gap between total balance and payment last month is much wider. Gen Xers report the widest gap, with a median outstanding credit card debt of $2,000 and a median monthly payment of $400.

Many factors contribute to Gen Z’s comparatively lower credit card debt: fewer fixed expenses in general at this stage of their lives, lower credit card limits that are typical of younger borrowers who are still establishing creditworthiness and leftover savings from pandemic stimulus payments that have helped them keep debt at bay. However, Gen Zers still deserve credit (pun intended) for staying on top of their debts. The youngest generation of adults seems to understand how to responsibly use revolving credit — that is, by effectively treating it as debit, or paying off as much of their balance as possible each month. They likely learned about the dangers of compound interest and are especially wary of carrying a balance in a rising-rate environment.

Gen Z’s credit card management is a bright spot amid wider financial concerns

Financial services leaders must remember that it’s not all sunshine and roses for Gen Zers as they begin their financial lives. The current macroeconomic environment and the toll of the coronavirus pandemic are still evident in Gen Z’s financial well-being struggles.

Gen Z adults feel their financial security is tenuous at best. Morning Consult’s Financial Well-Being Scale reveals that only 22% of them believe they could handle a major unexpected expense, and 39% say their finances control their life as of January. Their long-term outlook is suffering as a result: Less than a third of Gen Z adults (31%) say they are securing their financial future, and 32% believe that because of their money situation, they will never have the things they want in life.

Perhaps Gen Z adults are being too hard on themselves when thinking about their financial future. They appear to be starting off on the right foot in their credit journey, but leaders should nevertheless remain empathetic to the anxiety the youngest adults feel about their finances overall.